RBI is making it difficult for fintech firms

In today's newsletter we see how the RBI have introduced regulations that could affect many BNPL companies

Hello and Welcome to

Rise & Shine☀ - Sunday Edition,

Every Sunday, an email will arrive in your inbox detailing a specific topic to help you understand it better.

Let’s get started

On June 20, the RBI released a short circular address to all “Authorised Non-bank Prepaid Payment Instrument (PPI) Issuers.” It said, “The PPI-MD does not permit loading of PPIs from credit lines.”

Sounds quite confusing? Yeah, we know. But with that one line, the RBI sent India’s fintech companies into a tizzy.

So what’s PPI and why is this circular so damning? Well, let’s start from the top. How did “Buy Now Pay Later (BNPL)” companies actually come into existence?

Well, technically you could argue that it’s a 200-year-old idea roaring back to life. See sometime in the 19th century, a furniture dealer in New York City began selling goods on credit. Actually, it was in installments. And if you missed an installment, the seller would repossess your goods. However, the flexibility to pay monthly (on credit) was very enticing. But the monthly installment plan lost some of its sheens when credit cards rolled around during the same time.

And soon enough, credit cards began dominating the finance industry. But then, some industrious folks revised the old “installment” ideal. They stepped up and began offering “zero interest” loans to customers. They’d partner with certain merchants and work out a very interesting deal. Say somebody wanted to make a purchase of ₹1,000, the BNPL company would promise to take care of the bill at no cost. And then they’d ask the customer to pay back the sum in 15 days or even split it into installments over a 3–6 month period. They’d tell the customer they wouldn’t charge interest.

On the backend, they’d pay the merchant almost immediately. But instead of settling the full ₹1,000, they’d pay something like ₹950 and pocket the difference. The merchant agrees to take the hit because they can push the purchase almost immediately. It works in their favor too.

And for consumers who did not have access to a credit card, this seemed like quite a fantastic idea. In fact in India alone, the BNPL industry soared by a staggering 569% in 2020 and 637% in 2021.

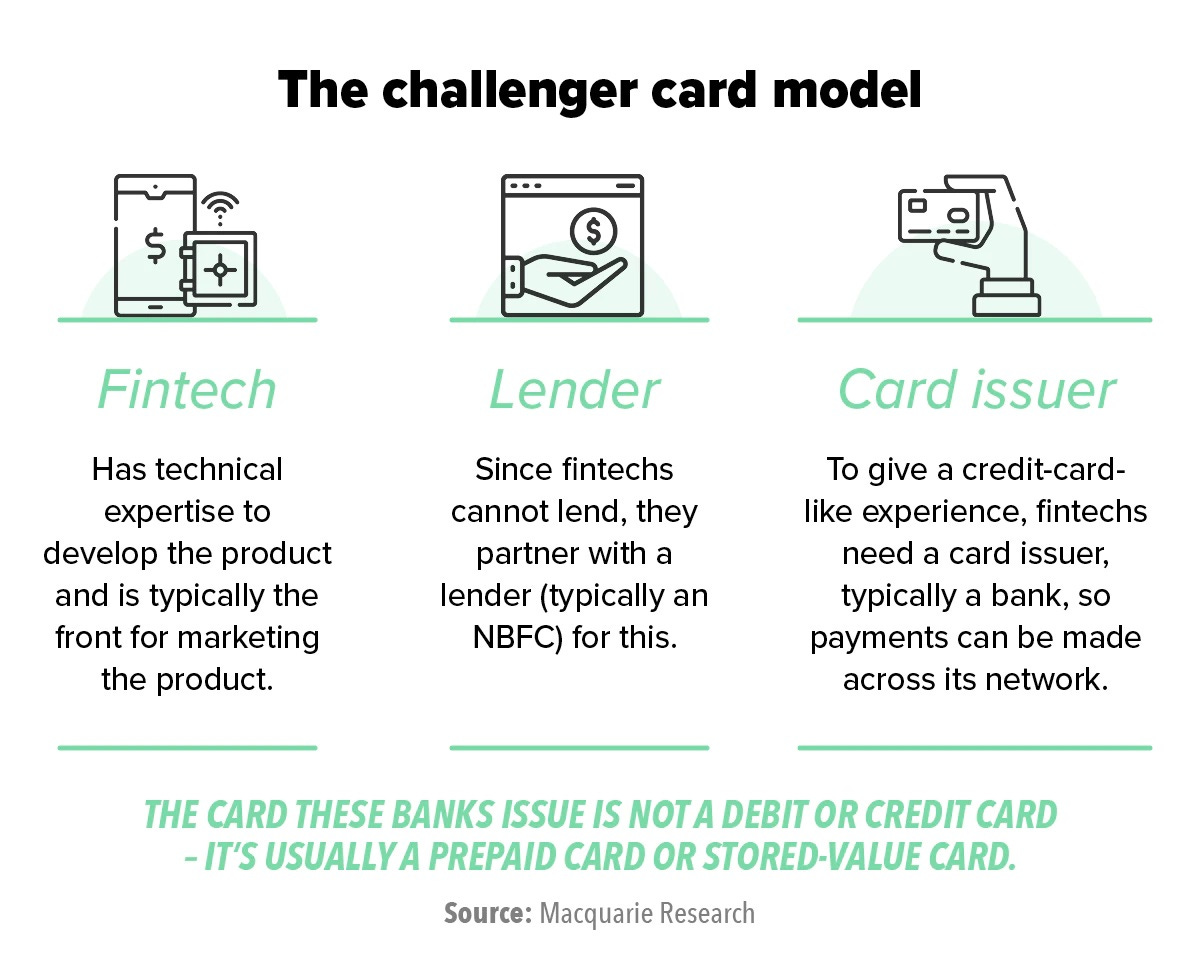

But then, some of these BNPL companies decided that they were actually “credit card challengers”. They weren’t just in the lending business. They felt the urge to replicate the feel of a credit card. They wanted to issue physical cards that you could slip into your wallet and swipe even if you went into a kirana store to pick up some groceries.

But there was a bit of a conundrum. You see, the RBI only allows licensed banks to issue credit cards. The regulator doesn’t even allow large non-banking finance companies (NBFC) like Bajaj Finance to issue one. So BNPL companies went to their conference rooms and thought and thought some more…how could they get around these regulations? And suddenly, the answer appeared — Prepaid Payment Instruments.

We have posted a reel explaining the guidelines imposed by RBI.

So what’s this PPI all about?

Well, think of PPIs as a digital wallet or card that functions like a mini bank account — like a gift card. You can top it up with money anytime using your bank account, debit card, or even a credit card. And then you use this “stored” money to make any purchase you want.

But BNPL companies wanted to add another feature on top. They wanted to load your wallet with credit from some other entity. So even if you couldn’t top it yourself, somebody else could do it for you, get it? So they partnered with folks holding a PPI licence. They then issued prepaid cards (like Slice), and topped it up using a credit line or a loan. And that credit line didn’t come from a bank. It came from an NBFC.

Take cards issued by Slice for instance. It struck a deal with the State Bank of Mauritius (SBM) which had a PPI license. They could issue a card now. And then, Slice used its own NBFC — Quadrillion Finance to top up the card with a loan. Consumers think they’re using a credit card. It looks and feels like one. But if somebody defaults, it’s Slice and the NBFC partners who are left licking their wounds. Not SBM. The bank had just lent its name for the purpose of issuing a card and that’s about it.

This jugaad (innovative approach) bypassed the formal banking system altogether and the RBI doesn’t seem to like it all that much. After all, some reports suggest that fintech firms have been issuing nearly 2 million of these pseudo credit cards a month when compared to the 1.5 million credit cards issued by banks. You can see why the banking regulator finally felt the need to do something.

So what does this circular from the RBI really mean then?

Well, most experts think that fintech companies will no longer be able to use their lending partners to top up consumer wallets. It doesn’t matter even if the card has the backing of a bank. So if you take Slice as an example again, they might have to take Quadrillion Finance out of the equation and ask SBM very nicely if the bank would be willing to act as both a card issuer as well as a lending partner for Slice.

The RBI’s latest fintech regulation – which bars non-banks from loading their credit lines onto wallets and prepaid cards – could have an adverse impact on fintech companies while benefiting banks, according to a report by Macquarie Research.

Big numbers: According to the Macquarie report, some new-generation firms were adding 200,000 to 300,000 cards using prepaid payment instrument (PPI) licenses and loading users' wallets with credit lines from banks, non-banks, and other financial institutions.

Credit card startups like Tiger Global-backed unicorn Slice and Uni Cards are likely to be hit hardest by RBI’s move.

3 months to iron out issues: The RBI wants the stakeholders to use the time to get ready for handling tokenised transactions, processing transactions based on tokens and implementing alternate mechanisms to handle post-transaction activities.

It also wants them to generate adequate public awareness about creating the tokens and using them effectively during transactions.

Though creating tokens is voluntary for the cardholders, the central bank has encouraged cardholders to tokenise their cards for their own safety. However, those who do not wish to create a token can continue to transact by entering card details manually during the transaction.

What is tokenisation? Tokenisation entails replacing the card details with a unique code or token, allowing online purchases to go through without exposing sensitive card details. To date, about 19.5 crore tokens have been created.

Have you checked our reel explaining the guidelines imposed by RBI?

Hit 💜, if you enjoyed the article. You can forward this mail or share it on social media.